Inflation might have fallen off the list of concerns for many investors, but history suggests that failing to protect against it could be hazardous to your wealth.

Inflation fears are out of fashion within the investor community. They’re far more interested in recession spotting and next year’s presidential election.

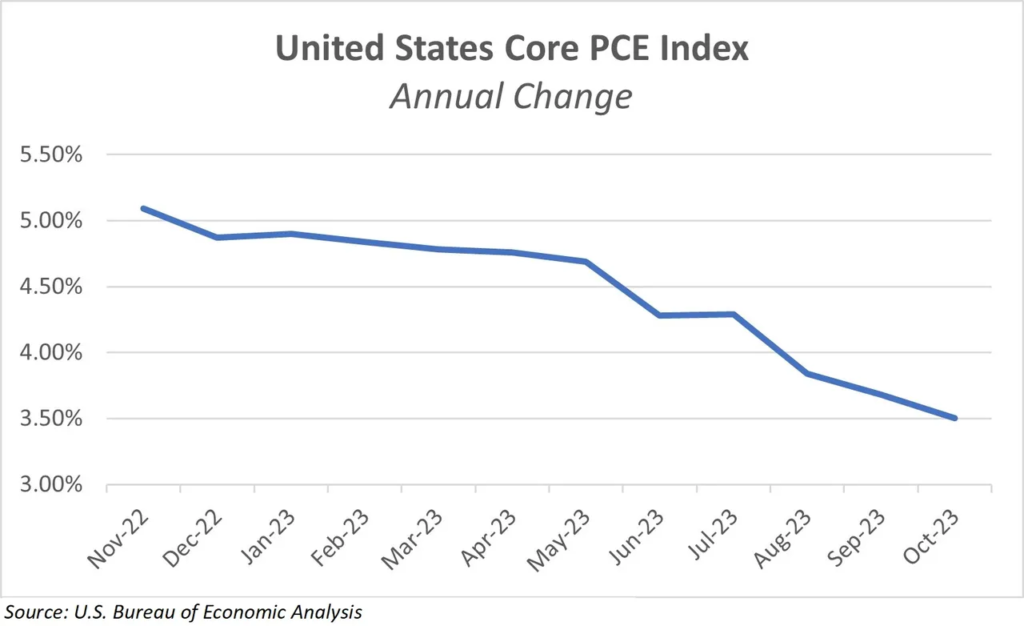

After all, the core Personal Consumption Expenditures (PCE) Index, the Federal Reserve’s preferred measure of inflation, has declined steadily over the past 12 months. “Core” simply means that food and energy prices are stripped out of the index because they tend to be volatile in the short term and can be driven by environmental issues or geopolitics.

While I’d certainly rather see inflation rates declining rather than accelerating, such charts can be misleading. Ultimately, we’re still talking about inflation growth (just a slowing rate of that growth). Inflation is commonly reported by comparing the rate of inflation growth against the previous year. While the chart above demonstrates that the rate of inflation is declining, there is still inflation! Prices are still going up. Goods and services still cost more. Inflation is still chipping away at the purchasing power of your dollars.

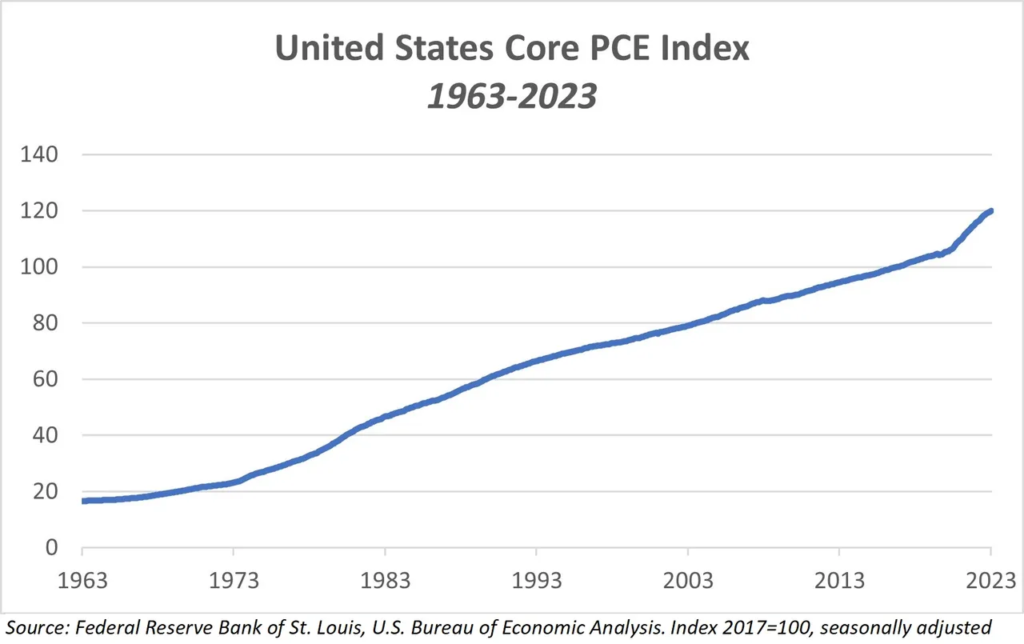

Here is another way to think about inflation. We’re looking at the same core PCE price index from the first chart. But rather than comparing year-over-year growth, we’re simply looking at how the index has behaved over the past 60 years.

You’ll be hard-pressed to find a period when the United States had deflation. That’s because in 60 years, it hasn’t happened. To be fair, the “headline” PCE, which includes food and energy prices, did have a modestly deflationary period in 2009 after the Great Financial Crisis.

Regardless of how you choose to measure inflation, it is ubiquitous in our modern economy. Sometimes you feel it. Sometimes it is more stealthy. But it is always eroding your purchasing power by degrading the value of your hard-earned dollars over time.

When we think about wealth preservation, it would be shortsighted to simply consider present circumstances. If we look just beyond our horizon to the near future, there is a very real possibility that inflation rates pick back up. Several factors, including spending on decarbonization, reshoring manufacturing, increased military spending and a shortage of labor can all pressure prices upward.

Maybe we will experience another spike in inflation. Or perhaps inflation goes unnoticed with low-single-digit growth over a prolonged period — the proverbial boiling frog scenario.

What we do know is clear: Inflation is not going away. Your choice is how you let it impact your wealth. You can let it ravage your savings, or you can protect your portfolio and retirement with these three simple steps:

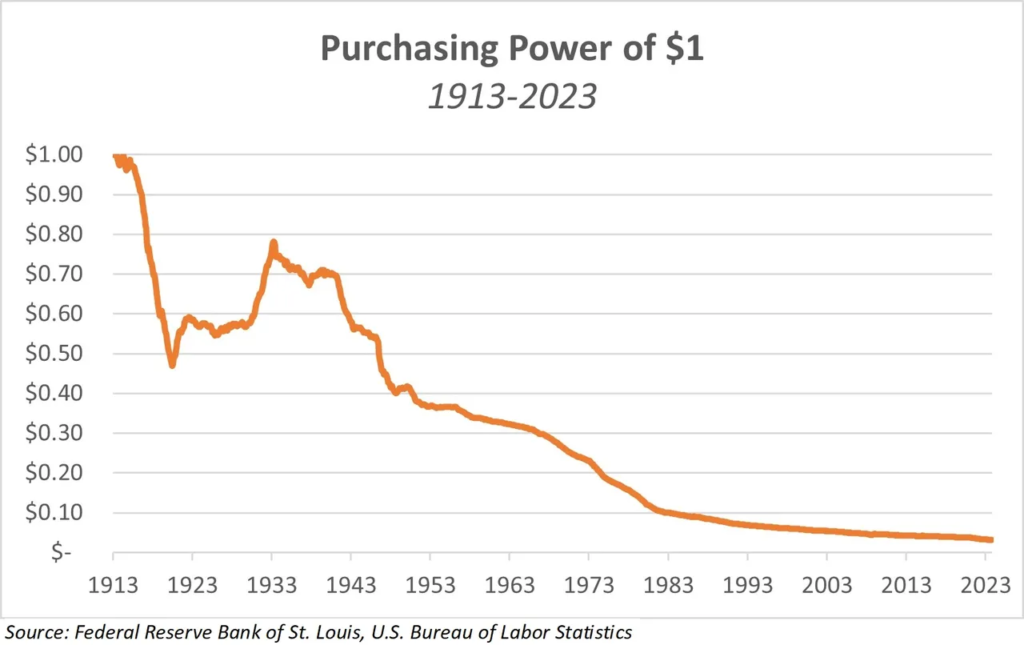

By definition, inflation is an increase in the price of goods and services. The more inflation there is, the less your cash can buy. That is to say, the purchasing power of the currency is reduced. We know that inflation has been a constant force for several decades. The chart below is a different way to think about the impact of inflation over the years. It may hit close to home.

The purchasing power of the U.S. dollar has steadily decreased over the last century. That’s what inflation does to fiat currencies like the dollar over time. The solution here is pretty simple. Beyond having some cash on hand to meet expenses, get through an emergency or as dry powder for some opportunistic investing, you should avoid having excessive amounts of cash as part of your long-term strategy. Having dollars stuffed under a mattress or locked up in a safe or bank vault is not an effective way to beat inflation.

OK, there are exceptions. I don’t recommend filling your home with refrigerators or bowling balls. But the point is to own real assets. Real estate is a typical example of this strategy. However, with residential real estate affordability near a 40-year low and the office space struggling, I’m less enthused with the sector beyond a few niche areas.

Thankfully, there are other options. I’ve already professed my love for pipelines, in my article These Energy ‘Middlemen’ Are an Income Lover’s Dream. The midstream companies that own them have already spent big bucks to build out their infrastructure. Inflation should increase the value of these assets as they become increasingly more expensive to replace.

Gold is another way to protect yourself from the wealth-eroding powers of inflation. There are several different ways to invest. You might choose to own the physical metal, big gold mining companies, junior miners or gold royalty companies. They all perform differently depending on the environment. That’s why my firm, SAM, has multiple strategies with a gold weighting component.

But no matter how you choose to get your gold exposure, its track record as a store of value over thousands of years means the odds of maintaining your purchasing power in the face of inflation are in your favor.

OK, there are exceptions. I don’t recommend filling your home with refrigerators or bowling balls. But the point is to own real assets. Real estate is a typical example of this strategy. However, with residential real estate affordability near a 40-year low and the office space struggling, I’m less enthused with the sector beyond a few niche areas.

Thankfully, there are other options. I’ve already professed my love for pipelines, in my article These Energy ‘Middlemen’ Are an Income Lover’s Dream. The midstream companies that own them have already spent big bucks to build out their infrastructure. Inflation should increase the value of these assets as they become increasingly more expensive to replace.

Gold is another way to protect yourself from the wealth-eroding powers of inflation. There are several different ways to invest. You might choose to own the physical metal, big gold mining companies, junior miners or gold royalty companies. They all perform differently depending on the environment. That’s why my firm, SAM, has multiple strategies with a gold weighting component.

But no matter how you choose to get your gold exposure, its track record as a store of value over thousands of years means the odds of maintaining your purchasing power in the face of inflation are in your favor.

Michael is a Portfolio Manager and Deputy Chief Investment Officer at Stansberry Asset Management. His duties include sourcing investment opportunities and conducting ongoing due diligence across SAM’s portfolios. Michael co-manages our Income and Tactical Select strategies.